Weekly PROPHET NOTES 3/24/25

Global Outlook: Talking the talk, but walking the talk...?

Welcome to another week, sponsored by Ukraine war talks in Saudi Arabia. Yes, once again US Inc. will meet with Russia and then with Ukraine, after which we should get just enough headlines to get us through the week. Only headlines, because nothing will be achieved in the talks.

Fundamentals remain unchanged, the energy infrastructure ceasefire is still not confirmed while the timelines are getting shorter and shorter. Prediction market traders now have little doubt that the war will go on throughout the 20th of April deadline:

Well, as long as there is an ample amount of exit liquidity on these markets, I am happy.

Before we start, I’m making a small change to the format - the Markets section f this article will be moved to a separate piece on Tuesday, where I aim to detail my moves from the previous week with rationale rather than purely new markets. So starting from today, this article will feature only the outlook and remain completely free.

With that being said, Subscribe below if you hadn’t and let’s see what the future holds.

Weekly Outlook

I have quite a bit to unpack here so without further ado.

US Inc.

Shortly after the news on the proposed 30-day ceasefire hit the media, Trump had a call with his buddy Putin, during which they preliminarily agreed to a 30-day energy infrastructure strikes ceasefire.

We are here now a week later and this ceasefire is nowhere to be seen as neither side has officially agreed to it. The strikes continue and the proposal is slowly being forgotten. Maybe today’s talks will change it, but traders remain unconvinced:

I also don’t expect much from the talks, maybe a preliminary agreement on safe passage for commercial vessels on the Black Sea. And anything next will need to be approved by Ukraine as well, especially since Europe is taking a different approach on the war and pledges long-term military support. Ceasefires are no real estate deals. I will provide my update on the results of the talks on X as soon as news hit the wire.

Speaking of conquest, a delegation of American officials, including the Second Lady and Mike Waltz will travel to Greenland this week, supposedly to learn some of the island’s history and attend a dogsled race. While the incoming PM of Greenland is officially agains the acquisition, I expect there will be some conversation behind closed doors on American aims and how Greenland can accommodate them. I still believe that an outright acquisition is unlikely, but some special economic / military zone could be enough for Trump to achieve his goals.

Turning towards domestic issues, the biggest headline of the last week was deportation of alleged gang members to El Salvador prison. While the judge blocked the deportation, Trump’s team said that the plane is over international waters so they have no obligation to turn it around. With deportations going slower than expected, we can count on Trump to bend the law to achieve his goals.

The Americas

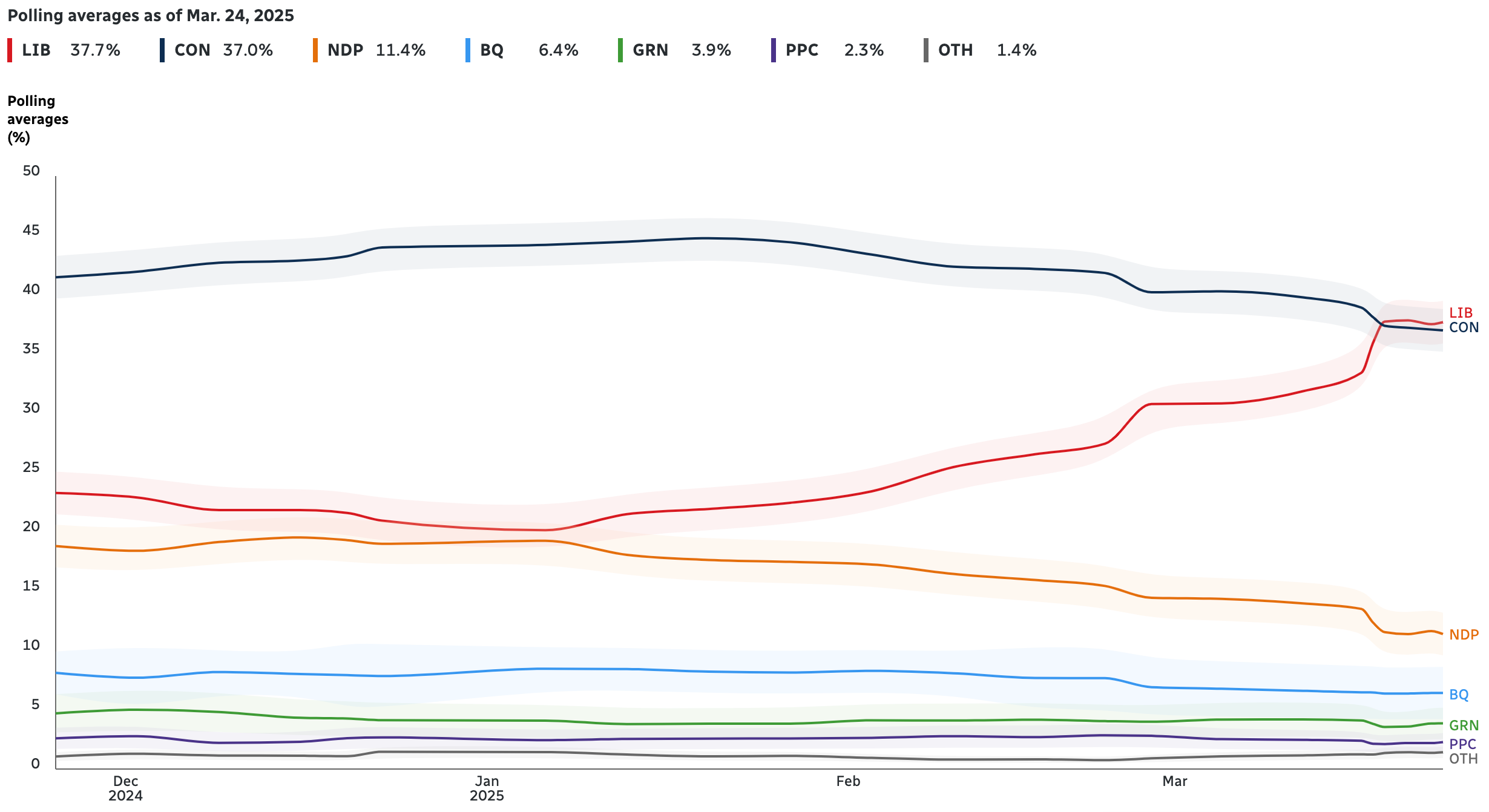

Election season is back. New Canadian PM has dissolved the parliament triggering a snap election. Due on the 28th of April, after which we have the Polish presidential election. However, the Canadian one is going to be more interesting with Liberals and Conservatives going head to head in the recent polls:

I’m not sure yet if there is any alpha to be had, but I’ll know soon enough!

Asia

The Yoon drama continues in South Korea, where the Constitutional Court is still yet to decide on the president’s impeachment. In the meantime, it has reinstated Han Duck-soo, the prime minister, as acting president. He was previously suspended for his alleged role in the coup and for failing to fill three vacancies in the Constitutional Court. Well, the impeachment decision is supposedly imminent, let’s wait and see, my No position on Yoon being reinstated is still on.

Middle East & Africa

As usual, major news from this region. The main being that the Gaza ceasefire is no more. Israel, supposedly discouraged by lack of progress in negotiations with Hamas, decided to continue its campaign and complete all its goals. I said in the beginning that structuring of the deal is tragic and now we have the effects. Structuring deals was my job and I got paid handsomely to ensure they were good. Take a look yourself:

Anyone who thinks that some kind of ceasefire is still on the table I wish good luck. With Trump as president, there is more chance for a direct confrontation with Iran than another dismal ceasefire deal:

More on this market (and other Gaza ceasefire markets) tomorrow.

Take it a bit as a joke, but it seems that Israel just likes to shoot and once it starts, it’s really hard to stop. Because just after Gaza, it started to strike Southern Lebanon. And all of this is on top of regularly striking Syria. Jokes aside, Hezbollah is hardly a threat now so I don’t expect the second front to open anytime soon.

Moving a bit south, the operation against the Houthis continues with no tangible results to be seen. If anything, the controlled leak of internal comms made more fuss than the actual operation. And the leak was mostly targeted towards Europe, maybe even regarding the White Paper I detailed yesterday. Because if I were Trump, I’d take the White Paper as a direct rejection of my peace effort. More on X.

Moving to the perpetually neglected continent of Africa, it seems that the Africans are more focused on business than Team West - after a round of negotiations in Qatar, Congo and Rwanda are seemingly nearing an agreement on the violence there - it is all about the resources, so expect a quiet announcement of a minerals deal if everything goes right.

And lastly, update on Sudan, where a civil war is ongoing. The Sudanese army recaptured the presidential palace in Khartoum, potentially making a major advancement towards ending the war. I wouldn’t keep my hopes high though - African countries are extremely unstable. Trust me, I did business there and it was never pretty.

Europe

As a European, I’m always sad writing this segment. It seems that always I’m criticizing the leadership and I can never say a good word.

But maybe today. At least one piece. Germany has voted to exempt most of defense spending from debt restrictions. The most feared country in Europe is rearming hard with EUR 500 billion infrastructure fund. At least this time they seem to be on the good side.

Going back to usual programing, Turkey is undergoing some major unrest after Ekrem Imamoglu, the mayor of Istanbul was arrested. A likely opposition candidate for the upcoming presidential election, it is believed that this is an operation of Erdogan aiming to trump the opposition. The public is protesting wildly, but I expect Erdogan to prevail once again. It’s hardly the hardest challenge to his authority if you remember the recent military coup.

From less important news, there was a fire at Heathrow Airport that knocked down electricity for a extended duration, but the culprits are still unknown. Besides major airline delays, nothing much happened.

Lastly, after many proclaiming his expected death, Pope Francis seems to have come out on top out of double pneumonia. He looks feeble, but alive.

Business, Finance & Economics

A lot to unpack here as well as it was interest rate week. Starting from US Inc. Powell decided to leave the rates unchanged despite Trump’s pressure. The Fed is in a bit of a pickle as it expects the economy to slow down to 1.7% growth in 2025 while it also expects the inflation to average 2.7% (growth down from 2.1% in the previous forecast while inflation is up from 2.5% in the previous forecast). Tough one for the Fed, especially considering that Trump want s to refinance on the long-term bonds.

Luckily, the Bank of Japan is keeping their rates steady. The reverse carry trade will wait a bit more, but it’s coming.

Meanwhile in China we got a mix of success and problems. On the one hand BYD is making record highs, taking demand from Tesla on the announcement of new battery-charging tech while on the other hand the Chinese government is eyeing cosumer demand boos by raising the minimum wage, expanding the workfare programs and enabling subsidized credit for thrifty consumers. Details are remaining to be seen, but I would call Chinese doomers way too early.

Lastly, heading back to US Inc., Google has made its biggest acquisition to date, purchasing Wiz, a cuber security startup having contracts with AWS and Azure, for $32 billion. Flop? Maybe, but it remains to be seen. It’s surely a profitable business.

Wrap up

That’s all for the week. While we are waiting for insights on Ukraine talks, I’ll be prepping the market rundown for tomorrow.

In the meantime stay strong and we will see each other soon!

This is not official investment or life advice. Do your own research. This are only my opinions and I encourage anyone to do their own research before putting any money anywhere.